Andrew Cochrane, A revered figure in medicine had a momentous experience in 1956. His dermatologist suspected cancerous growth basis spots on his back, pathologist confirmed it as basal cell carcinoma which was promptly removed but and Andrew still went ahead to consult a specialist.

The specialist discovered a lump in his right armpit and advised removal. Surgery was booked and while the specialist informed Andrew at the end that he has done his best to remove the cancerous cells, the prognosis was grim and it seemed Andrew didn’t have much to live.

Alas the specialist was wrong, there was no cancer, as the pathologist confirmed after evaluating the tissue removed during surgery.

Andrew later said “I didn’t doubt the surgeon’s words”.

Unfortunately Andrew didn’t think, decided too quickly and by the time he realized his mistake it was too late.

This coupled with delay in changing your mind can aggravate the situation

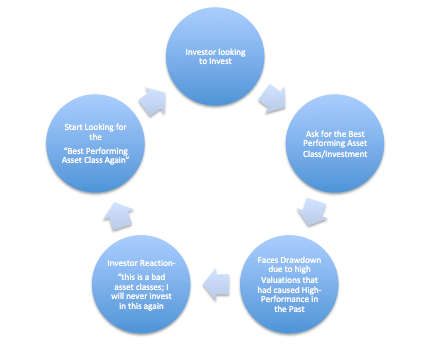

Typical Investor Decision-Making Cycle

Investors find it easier to blame everyone and everything except for their own decision-making process.

Advisors driven by revenue-considerations often fail to challenge and end up supporting the outcome-oriented approach of the client failing to address the risk-reward of the decision.

How to Think?

As Geoffery Caveney points:

Robert Shiller’s Cyclically Adjusted Price to Earnings (CAPE) ratio is now around the level of 1929, and it was only higher in the late 90s dot-com bubble.

Many commentators have pointed to this indicator recently as a danger sign for the stock market.

However, this is misleading right now because the CAPE ratio’s 10-year back period begins with the Great Recession in 2007.

If you had used this as an indicator you would have probably exited equities in early 2017, however that would also meant losing the fantastic returns of 2017 and first half 2018.

As pointed by Michael Batnick, if you look at a simple strategy of buying when index is below average CAPE ratio and sell when it’s above, this is how it turned out:

1926-55-same return as buy & hold-9.9%

1955-till today- Buy & Hold 10.2% Vs. Above/below CAPE-7.3%

What gave-while from 1926-55, the above strategy would have kept you invested 68% of the time from 1955-till today, it kept you invested only 25% of the time.

Clearly this explains a lot on “timing strategies” that a lot of investors use as a “rule of thumb”

Think Differently

This needs the investor to think very differently about their investment decision-making.

Here are some points to consider:

- Use your past experience to understand the gaps in decision-making rather than a judgment call on the asset-classes;

- Remember asset-classes work in cycles; so don’t congratulate yourself for a right decision or curse yourself for a wrong one; Perhaps the only thing that worked for you was catching one cycle while missing other one; Use that learning to understand cycles before taking a decision;

- Bit of looking behind and a bit of crystal ball grazing;

- Evaluate current risk-reward;

- Understand the investment process of the investment under consideration;

- Look at recent past outcomes to evaluate over-heating in the underlying portfolio to evaluate value consideration and whether the underlying is already pricing in future growth or not;

- Ask your advisor for opportunities which have under-performed or neutral performed to understand future trends; Ask about the quality of the underlying;

- Retain objectivity and be dispassionate

Most importantly – leave the baggage behind unless you know something that’s others don’t and that’s based on facts not feelings;

____________________________________________________________________________________________

Nice sir,

Very informative

LikeLike