Over the last 1-year investors in equities have experienced a virtual roller-coaster rise.

The markets went down over 35% in a matter of no time and them doubled from the bottom foxing several investors.

During this up and down, we got to spare a thought for the fixed income investor who has found nowhere to hide.

The part of the market perceived to be safe has no yields available while another part of the market, investors have been too scared to invest in.

This also has to be seen in the context of investors in AT-1 bonds of banks like Yes and LVB losing everything thereby creating heightened risk aversion.

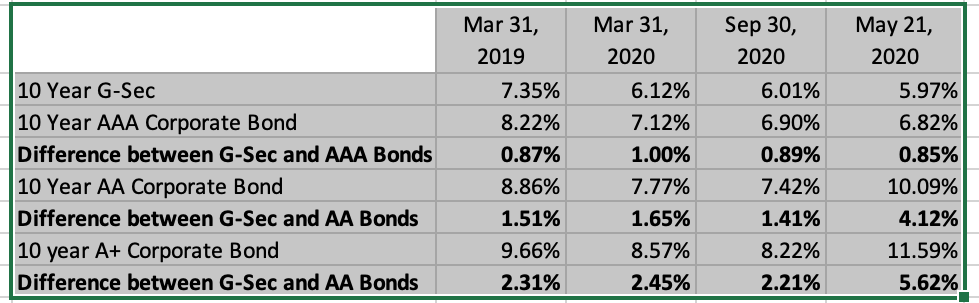

The heightened risk aversion can be seen in interest rates lower than the 10-Year Govt Security for the AAA rated companies.

In the meanwhile, the Reserve Bank of India devised a strategy to keep the interest rate that the Govt. pays on its bonds anchored to an artificial 6% yield.

Reserve Bank infact used every tool available in the arsenal to keep interest rates at or below 6%.

When the 2nd wave hit the country, this 6% anchor virtually rendered the 10-year govt security being used a benchmark irrelevant as clear from the data below:

While the yield difference between 1- Year Govt. Security and AAA bonds has remained steady, the yield difference between Govt. Security and AA/A rated bonds is not at all-time highs.

One of the reasons for the AAA yields have remained steady of-course is their safe haven status and the massive deleveraging in some of the large AAA entities.

However, the All-time high yield differential between below AAA securities and the benchmark 10-year GOI paper, raises a question mark on the 10-Year Govt. Security’s status as a benchmark.

This is also the time when a fixed Income investor should be looking to make the most of the situation to lock in yields.

As per Crisil default study 2020, here are the average default rates for AA and A rated bonds from the CRISIL universe of rated companies:

| Rating | No. of Companies | 1-Year | 2-Year | 3-Year |

| AA | 28000 | 0.08% | 0.22% | 0.31% |

| A | 54000 | 0.21% | 0.90% | 1.76% |

This extremely low default rate must give confidence to fixed income investors to take exposure to accrual funds of mutual funds to lock-in the higher yields.

Pandemic ensured that a lot of companies have already not only seen the worst but have even fortified their balance sheet on the back of some good earnings, debt paring and conservatism.

Infact the commentaries from major banks like HDFC and ICICI iterated that their corporate portfolios are less likely to default as 80-90% of the same is A or above rated showing the strength of companies rated A.

As per Mr. N. Sivaraman, MD, ICRA the expectation of large-scale defaults owing to the second wave are low and one of the reasons is how corporates have worked on raising capital and deleveraging in last 1 year to strengthen their balance sheets especially in the traditionally vulnerable sectors like commodities where pent-up demand has led to record profits even after deleveraging.

The anomaly created by this artificial anchoring of 10-year Govt. Bond by the Reserve Bank is a golden chance for fixed income investors who have been wondering lost for last over 12 months to play smart and fortify their asset allocation.